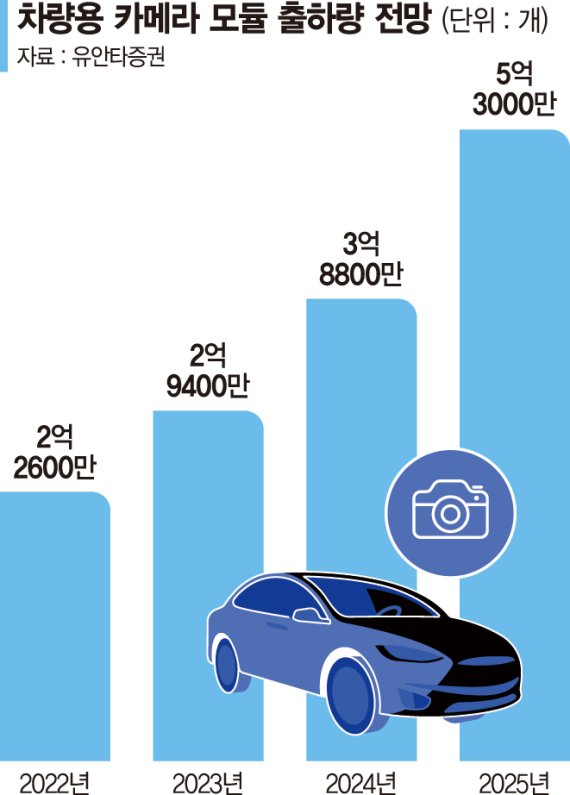

자율주행차 시장은 미래 모빌리티 산업을 이끌 핵심 기술 분야로 주목받고 있다. 세계적으로 완성차 업체와 IT 기업들이 자율주행차 기술 개발에 막대한 투자를 단행하고 있으며 정부 차원에서도 관련 인프라 구축과 제도 정비를 추진하고 있다. 자율주행차 시장은 미래 모빌리티 산업을 이끌 핵심 기술 분야로 주목받고 있다. 세계적으로 완성차 업체와 IT 기업들이 자율주행차 기술 개발에 막대한 투자를 단행하고 있으며 정부 차원에서도 관련 인프라 구축과 제도 정비를 추진하고 있다.

interspective sgn, 출처 스플래시 해제 interspective sgn, 출처 스플래시 해제

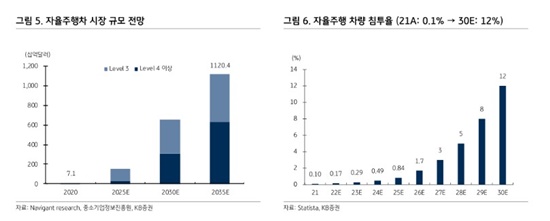

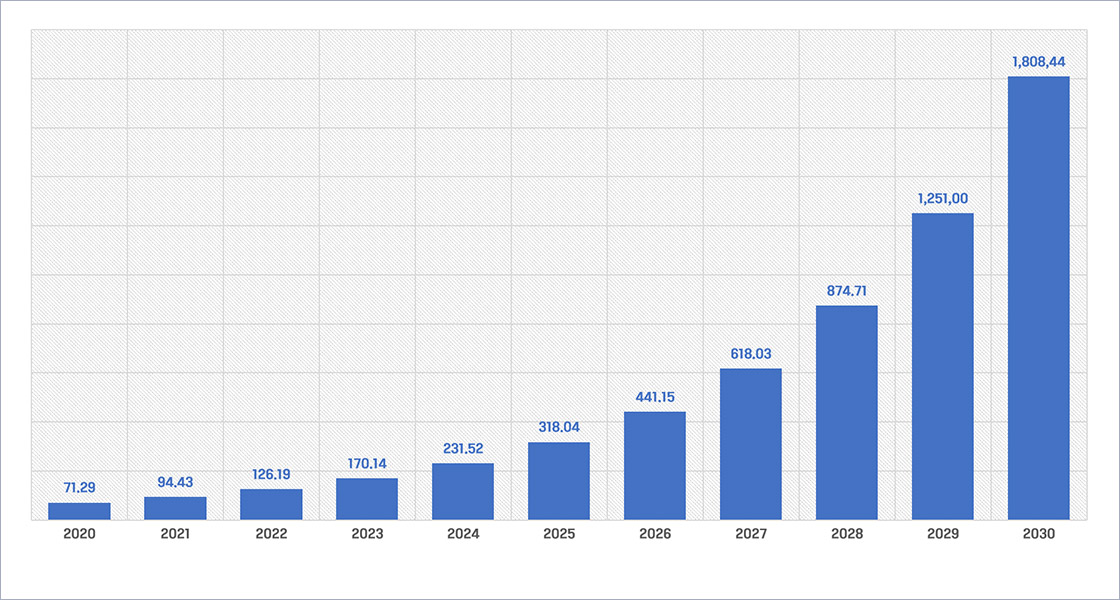

시장조사기관들은 자율주행차 시장이 앞으로 급성장할 것으로 전망하고 있습니다. 2022년 약 28억달러 규모에 불과했던 시장이 2030년에는 557억달러를 웃돌 것으로 전망됩니다. 완전 자율주행차 상용화가 본격화되면서 새로운 모빌리티 서비스와 부가가치 창출 기회도 열릴 것으로 기대되고 있습니다. 그러나 자율주행차 기술의 상용화 시기와 시장 성장 속도에 대해서는 여전히 불확실성이 존재합니다. 기술적 난제 해결과 법·제도적 기반 구축, 인프라 구축 등에 시간이 걸릴 수 있기 때문입니다. 본 포스팅에서는 자율주행차의 시장 규모와 성장 잠재력을 다각도로 분석하여 시사점을 도출해보고자 합니다. 1. 자율주행차 시장의 현황과 전망입니다 시장조사기관들은 자율주행차 시장이 앞으로 급성장할 것으로 전망하고 있습니다. 2022년 약 28억달러 규모에 불과했던 시장이 2030년에는 557억달러를 웃돌 것으로 전망됩니다. 완전 자율주행차 상용화가 본격화되면서 새로운 모빌리티 서비스와 부가가치 창출 기회도 열릴 것으로 기대되고 있습니다. 그러나 자율주행차 기술의 상용화 시기와 시장 성장 속도에 대해서는 여전히 불확실성이 존재합니다. 기술적 난제 해결과 법·제도적 기반 구축, 인프라 구축 등에 시간이 걸릴 수 있기 때문입니다. 본 포스팅에서는 자율주행차의 시장 규모와 성장 잠재력을 다각도로 분석하여 시사점을 도출해보고자 합니다. 1. 자율주행차 시장의 현황과 전망입니다

인기글

현재 자율주행차 시장 규모, 현재 자율주행차 시장은 초기 단계로 2022년 기준 약 28억달러 규모다. 완전 자율주행차(레벨 4-5)는 아직 상용화되지 않았지만 부분적 자율주행 기능을 탑재한 차량이 일부 출시되고 있다. 주요 자동차 업체들이 자율주행차 개발에 막대한 투자를 단행하면서 기술 경쟁이 가열되고 있다. 향후 시장 성장 전망과 연평균 성장률 전문가들은 자율주행차 시장이 급성장할 것으로 전망하고 있다. 스태티스타에 따르면 2025년에는 260억달러, 2030년에는 약 557억달러 규모에 이를 전망이다. 연평균 성장률도 2025년까지 39%, 2030년까지 25%에 이를 것으로 예상된다. 완전 자율주행차 상용화가 본격화되면 시장은 더욱 빠르게 성장할 것으로 보인다. 주요 성장 동인 분석 자율주행차 시장의 성장을 견인할 주요 동인으로는 첫째, 안전성과 편의성 향상에 대한 수요 증가가 꼽힌다. 둘째, 정부의 자율주행차 육성 정책과 기술 로드맵 수립 등 제도적 기반 마련이 시장을 뒷받침한다. 셋째, IT기업과 자동차업체 간 기술협력으로 혁신이 가속화되고 있다. 넷째, 카셰어링 등 새로운 모빌리티 서비스 수요 증가도 시장을 부양할 전망이다. 2. 자율주행차 기술 발전 속도 현재 자율주행차 시장 규모, 현재 자율주행차 시장은 초기 단계로 2022년 기준 약 28억달러 규모다. 완전 자율주행차(레벨 4-5)는 아직 상용화되지 않았지만 부분적 자율주행 기능을 탑재한 차량이 일부 출시되고 있다. 주요 자동차 업체들이 자율주행차 개발에 막대한 투자를 단행하면서 기술 경쟁이 가열되고 있다. 향후 시장 성장 전망과 연평균 성장률 전문가들은 자율주행차 시장이 급성장할 것으로 전망하고 있다. 스태티스타에 따르면 2025년에는 260억달러, 2030년에는 약 557억달러 규모에 이를 전망이다. 연평균 성장률도 2025년까지 39%, 2030년까지 25%에 이를 것으로 예상된다. 완전 자율주행차 상용화가 본격화되면 시장은 더욱 빠르게 성장할 것으로 보인다. 주요 성장 동인 분석 자율주행차 시장의 성장을 견인할 주요 동인으로는 첫째, 안전성과 편의성 향상에 대한 수요 증가가 꼽힌다. 둘째, 정부의 자율주행차 육성 정책과 기술 로드맵 수립 등 제도적 기반 마련이 시장을 뒷받침한다. 셋째, IT기업과 자동차업체 간 기술협력으로 혁신이 가속화되고 있다. 넷째, 카셰어링 등 새로운 모빌리티 서비스 수요 증가도 시장을 부양할 전망이다. 2. 자율주행차 기술 발전 속도

자율주행 레벨별 기술 발전 단계의 자율주행 기술은 레벨 0부터 5까지 6단계로 나뉜다. 현재 상용화된 기술은 레벨2 수준의 부분 자율주행이다. 레벨 2는 차량제어 중 세로(가속/감속) 및 가로(스티어링) 방향의 보조업무를 시스템이 한정적으로 실시한다. 레벨3(조건부 자율주행)는 기술적으로 개발이 많이 진행됐지만 아직 상용화되지 않았다. 레벨4(고수준 자율주행)와 레벨5(완전 자율주행)에 이르기 위해서는 센서, 소프트웨어, 차량 제어 등 다양한 분야에서 기술적 돌파구가 필요한 상황이다. 완전자율주행(레벨 4-5) 상용화 시기 전망, 완전자율주행차 상용화 시기에 대해서는 전문가들 사이에서 다소 의견 차이가 있다. 일부는 2025년께 레벨4 수준의 차량이 출시될 것으로 전망하고 있다. 그러나 대다수 전문가들은 2030년대 중반이 돼야 레벨4~5 차량이 본격적으로 상용화될 것으로 전망한다. 기술적 난제 해결과 법/제도적 기반 구축, 인프라 확충 등에 상당한 시간이 걸릴 것으로 보기 때문이다. 기술적 과제와 해결책의 완전 자율주행 실현을 위해서는 여전히 많은 기술적 과제가 남아 있다. 첫째, 센서의 인식 능력과 정확도를 높여야 한다. 둘째, 복잡한 상황 인지와 의사결정을 위한 AI 알고리즘 고도화가 필요하다. 셋째, 사이버 보안 강화와 안전성 검증 체계 구축이 과제로 지적된다. 이를 해결하기 위해 센서 융합, 딥러닝 기술 발전, V2X(차량-외부 통신) 기술 등의 발전이 요구된다. 또 자율주행 데이터 구축, 시뮬레이션 고도화, 오픈소스 활용 등 기술개발 인프라 확충도 중요한 과제다. 3. 주요 국가/지역별 시장 전망 자율주행 레벨별 기술 발전 단계의 자율주행 기술은 레벨 0부터 5까지 6단계로 나뉜다. 현재 상용화된 기술은 레벨2 수준의 부분 자율주행이다. 레벨 2는 차량제어 중 세로(가속/감속) 및 가로(스티어링) 방향의 보조업무를 시스템이 한정적으로 실시한다. 레벨3(조건부 자율주행)는 기술적으로 개발이 많이 진행됐지만 아직 상용화되지 않았다. 레벨4(고수준 자율주행)와 레벨5(완전 자율주행)에 이르기 위해서는 센서, 소프트웨어, 차량 제어 등 다양한 분야에서 기술적 돌파구가 필요한 상황이다. 완전자율주행(레벨 4-5) 상용화 시기 전망, 완전자율주행차 상용화 시기에 대해서는 전문가들 사이에서 다소 의견 차이가 있다. 일부는 2025년께 레벨4 수준의 차량이 출시될 것으로 전망하고 있다. 그러나 대다수 전문가들은 2030년대 중반이 돼야 레벨4~5 차량이 본격적으로 상용화될 것으로 전망한다. 기술적 난제 해결과 법/제도적 기반 구축, 인프라 확충 등에 상당한 시간이 걸릴 것으로 보기 때문이다. 기술적 과제와 해결책의 완전 자율주행 실현을 위해서는 여전히 많은 기술적 과제가 남아 있다. 첫째, 센서의 인식 능력과 정확도를 높여야 한다. 둘째, 복잡한 상황 인지와 의사결정을 위한 AI 알고리즘 고도화가 필요하다. 셋째, 사이버 보안 강화와 안전성 검증 체계 구축이 과제로 지적된다. 이를 해결하기 위해 센서 융합, 딥러닝 기술 발전, V2X(차량-외부 통신) 기술 등의 발전이 요구된다. 또 자율주행 데이터 구축, 시뮬레이션 고도화, 오픈소스 활용 등 기술개발 인프라 확충도 중요한 과제다. 3. 주요국/지역별 시장전망

kateboss5000, 출처Unsplash kateboss5000, 출처Unsplash

North America, Europe, and Asia are expected to be the leading markets for self-driving cars. The North American market is expected to reach about $200 billion by 2030. Europe is also under the leadership of the government in technology development and infrastructure construction, and the European market is expected to reach $150 billion by 2030. China is expected to become the largest market in Asia. Thanks to the Chinese government’s active support policy, the size of the Chinese market is expected to exceed $80 billion by 2030. Korea and Japan are also expected to emerge as promising markets based on the technology of finished car manufacturers and parts manufacturers. Comparison of government policies and legal/system-based comparison There is a difference between government policies and the level of establishing a legal/system-based foundation for commercialization of self-driving cars by country. Although the United States does not have federal-level unification regulations, it has a legal basis for self-driving tests and commercialization at the state level. The European Union has established an integrated regulatory system through cooperation between the Member States. China has established national development strategies and roadmaps, and is making policy efforts such as building test beds and supporting companies. South Korea is also pushing for related legislation and infrastructure creation plans with the goal of commercializing fully self-driving cars in 2027. U.S. companies such as Google Waymo, Tesla, and General Motors are leading the development of fully autonomous vehicles with technology and commercialization readiness of major companies. Weymo is leading the way in autonomous driving technology, and Tesla is pushing for commercialization of electric vehicle-based autonomous vehicles. GM is also aiming to launch a fully self-driving car in 2025. In Europe, finished car manufacturers such as BMW, Volkswagen and Daimler are speeding up the development of self-driving car technologies. While China’s Hyakudo and Tesla are leading the way in Asia, Hyundai Motor and Toyota are also improving their technology. In particular, IT companies are leading technological innovation in cooperation with automakers. 4. Changes in industrial ecosystems related to self-driving cars North America, Europe, and Asia are expected to be the leading markets for self-driving cars. The North American market is expected to reach about $200 billion by 2030. Europe is also under the leadership of the government in technology development and infrastructure construction, and the European market is expected to reach $150 billion by 2030. China is expected to become the largest market in Asia. Thanks to the Chinese government’s active support policy, the size of the Chinese market is expected to exceed $80 billion by 2030. Korea and Japan are also expected to emerge as promising markets based on the technology of finished car manufacturers and parts manufacturers. Comparison of government policies and legal/system-based comparison There is a difference between government policies and the level of establishing a legal/system-based foundation for commercialization of self-driving cars by country. Although the United States does not have federal-level unification regulations, it has a legal basis for self-driving tests and commercialization at the state level. The European Union has established an integrated regulatory system through cooperation between the Member States. China has established national development strategies and roadmaps, and is making policy efforts such as building test beds and supporting companies. South Korea is also pushing for related legislation and infrastructure creation plans with the goal of commercializing fully self-driving cars in 2027. U.S. companies such as Google Waymo, Tesla, and General Motors are leading the development of fully autonomous vehicles with technology and commercialization readiness of major companies. Weymo is leading the way in autonomous driving technology, and Tesla is pushing for commercialization of electric vehicle-based autonomous vehicles. GM is also aiming to launch a fully self-driving car in 2025. In Europe, finished car manufacturers such as BMW, Volkswagen and Daimler are speeding up the development of self-driving car technologies. While China’s Hyakudo and Tesla are leading the way in Asia, Hyundai Motor and Toyota are also improving their technology. In particular, IT companies are leading technological innovation in cooperation with automakers. 4. Changes in industrial ecosystems related to self-driving cars

koons, 출처 Unsplash koons, 출처 Unsplash

Influence of related industries such as automobiles, IT/SW, sensors, and infrastructure Self-driving cars are expected to affect not only the automobile industry but also various industries such as IT/SW, sensors, and infrastructure. First, in the automobile industry, the value chain is expected to be reorganized from the center of the existing internal combustion engine to the center of electric vehicles and autonomous driving technologies. The proportion of SW such as vehicle control and infotainment will increase significantly. Second, the IT/SW industry will see a surge in demand for technologies such as cloud, big data, and AI for autonomous vehicle operation. IT companies such as Google and Apple are actively entering the self-driving solution market. Third, the sensor and semiconductor industries are also expected to grow due to increased demand for self-driving car sensors and high-performance chips. Development of various sensor technologies such as LiDAR, radar, and cameras is essential. Fourth, related industries such as smart traffic lights, road sensors, and precision map data are also expected to emerge to build infrastructure for self-driving cars. New business models and service opportunity self-driving cars are expected to create new mobility service business models. Ride-sharing services such as Uber and Lift may be expanded to the base of self-driving cars. New services such as self-driving robots and unmanned shuttles will also be available. It is also expected that new value-added opportunities will be created using self-driving car data. There is a possibility that new businesses such as vehicle data-based insurance, entertainment, and advertising will emerge. The possibility of reorganizing the existing industrial value chain is highly likely to reorganize the existing automobile industry value chain on a large scale due to self-driving cars. Value is expected to move from hardware-centered to SW/data-centered. Cooperation with IT/SW companies is expected to be strengthened as vertical affiliations between finished car manufacturers and parts manufacturers are weakened. Competition between self-driving technology platform companies and service companies is also expected to intensify. In addition, if demand for individual vehicles decreases due to the spread of car sharing services, changes in the business model centered on automobile sales are expected to be inevitable. 5. Implications and investment strategies Influence of related industries such as automobiles, IT/SW, sensors, and infrastructure Self-driving cars are expected to affect not only the automobile industry but also various industries such as IT/SW, sensors, and infrastructure. First, in the automobile industry, the value chain is expected to be reorganized from the center of the existing internal combustion engine to the center of electric vehicles and autonomous driving technologies. The proportion of SW such as vehicle control and infotainment will increase significantly. Second, the IT/SW industry will see a surge in demand for technologies such as cloud, big data, and AI for autonomous vehicle operation. IT companies such as Google and Apple are actively entering the self-driving solution market. Third, the sensor and semiconductor industries are also expected to grow due to increased demand for self-driving car sensors and high-performance chips. Development of various sensor technologies such as LiDAR, radar, and cameras is essential. Fourth, related industries such as smart traffic lights, road sensors, and precision map data are also expected to emerge to build infrastructure for self-driving cars. New business models and service opportunity self-driving cars are expected to create new mobility service business models. Ride-sharing services such as Uber and Lift may be expanded to the base of self-driving cars. New services such as self-driving robots and unmanned shuttles will also be available. It is also expected that new value-added opportunities will be created using self-driving car data. There is a possibility that new businesses such as vehicle data-based insurance, entertainment, and advertising will emerge. The possibility of reorganizing the existing industrial value chain is highly likely to reorganize the existing automobile industry value chain on a large scale due to self-driving cars. Value is expected to move from hardware-centered to SW/data-centered. Cooperation with IT/SW companies is expected to be strengthened as vertical affiliations between finished car manufacturers and parts manufacturers are weakened. Competition between self-driving technology platform companies and service companies is also expected to intensify. In addition, if demand for individual vehicles decreases due to the spread of car sharing services, changes in the business model centered on automobile sales are expected to be inevitable. 5. Implications and investment strategies

AUTOMATIC DRIVERING VEHICLE AND ITS DIABILITY OF AUTOMOBILITY OF AUTOMOBILITY DATABILITY SERVICE AND ITSU,Cloud/Big Data Technology – Development – Dell™ technology-based business investment-based technology, including a commercial-based business-based data, including a commercialization and commercial designated data-based,INDOMATIC DRIVING AND ITS OPERATION METHOD FOR OPERATION OF INDOMATIC DRIVER MEDIMAGE # AUTOMOBUTOMOBUTOMO